Introduction: A Tale of Two Budgets

As U.S. households grapple with persistent inflation—from soaring housing costs to rising grocery bills—discretionary spending has tightened dramatically. Yet one category remains remarkably resilient: pet care. While Americans cut back on dining out (down 8% in 2024) and apparel (a 5% decline), they continue to invest heavily in their furry companions. In 2024, U.S. pet industry spending reached $1519 billion, boasting a 6-year compound annual growth rate (CAGR) of 9%—outpacing GDP growth by nearly 3x. What explains this unwavering commitment? Let’s dive into the data, behavioral science, and market dynamics driving this phenomenon.

📊 The Numbers: Pet Spending Resilience Amid Inflation

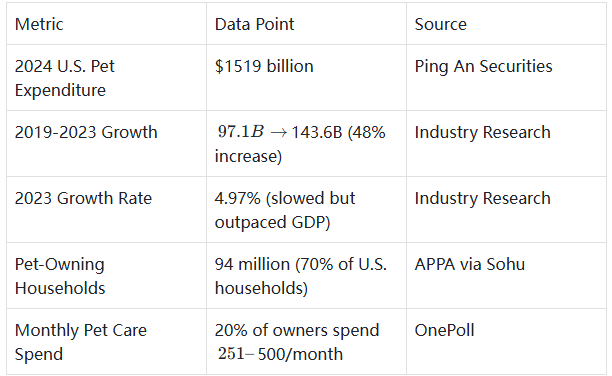

To grasp the magnitude of this trend, consider these key statistics:

Notably, even as inflation cooled pet food prices (0% YoY growth in April 2025), veterinary and service costs rose 4.6%—yet households didn’t abandon these expenses. Instead, they adapted their behavior, highlighting the “essential” status of pets in modern families.

🔍 Why Pet Spending Remains Non-Negotiable

1. Emotional Bond: Pets as Family, Not Luxuries

The primary driver is the psychological value of pet ownership. A University of Kent study found that owning a cat or dog boosts life satisfaction equivalently to earning $92,655 more annually—on par with the happiness gains from marriage. During economic stress, this emotional support becomes invaluable:

- 87% of pet owners describe their animals as “family members” (Civic Science poll)

- Pets reduce loneliness and stress hormones (cortisol) by 20–30%, per Harvard Medical School research

- Post-pandemic, 62% of owners report relying more on pets for emotional stability

This bond transforms discretionary spending into “essential” care. As Bank of America analysts note: “Pet owners prioritize their animals’ well-being over non-essential human expenses—viewing food, vet visits, and comfort items as basic needs, not indulgences”.

2. Rigid Demand: Non-Discretionary Pet Needs

Unlike travel or entertainment, core pet expenses (food, medical care, shelter) are inherently rigid. Even cost-conscious owners avoid cutting these:

- Pet food accounts for 52.8% of total spending, with 90% of owners refusing to compromise on quality despite price hikes

- Veterinary care remains a top priority: only 1% of households reduced vet visits in 2024, while pet insurance adoption surged 20% YoY (NAPHIA data)

- Essential services (grooming, boarding) saw only a 4% spending decline—far less than other service sectors

3. Consumer Adaptation: Trading Down, Not Opting Out

Instead of eliminating pet spending, Americans are optimizing their choices:

- 67% of dog owners adjusted their budgets by switching to value-priced food or buying in bulk

- 40% shifted purchases from specialty stores to grocery retailers for convenience and cost savings

- Premium brands like Hill’s maintained 19.5% YoY growth by implementing modest price increases (12% avg.)—proving brand loyalty for trusted products

- Smart pet products (e.g., automatic feeders) grew 18% YoY, as owners invest in long-term cost efficiency

4. Demographic Shifts: Millennials Drive Spending

Millennials—now the largest pet-owning cohort—prioritize pet welfare differently than previous generations:

- 67% of millennial owners spend more on pets than on themselves for discretionary items (Civic Science)

- Delayed marriage and children have led 45% of childless millennials to view pets as “furry kids”

- Urban millennials (in high-cost cities like Seattle/San Francisco) spend 30% more on pets than the national average, valuing companionship in small living spaces

📈 Market Implications: Resilience in Uncertainty

The pet industry’s resilience offers key insights for businesses and economists:

- Brand Power Matters: Top-tier brands (e.g., Hill’s, Chewy) retain pricing power, while value-focused products thrive in mid-market segments

- Service Innovation: Pet insurance (currently <1% penetration in the U.S.) and telehealth are fast-growing, addressing cost concerns

- Global Opportunities: Chinese manufacturers are gaining share in affordable pet supplies, leveraging supply chain advantages amid cost sensitivity

Conclusion: Pets as Economic Constants

In an era of financial uncertainty, American pet spending isn’t just a trend—it’s a reflection of shifting family structures and emotional priorities. As inflation persists, pets remain a “non-negotiable” expense because they provide irreplaceable emotional value, while owners adapt their behavior to maintain care standards.

For pet businesses, the takeaway is clear: prioritize value, emotional connection, and essential services to thrive. For economists, this trend underscores a broader shift in consumer values—where experiences and relationships increasingly outweigh material goods.

What’s your experience with pet spending during inflation? Share your thoughts in the comments or tag a fellow pet parent who’s made similar budget choices!